Introduction

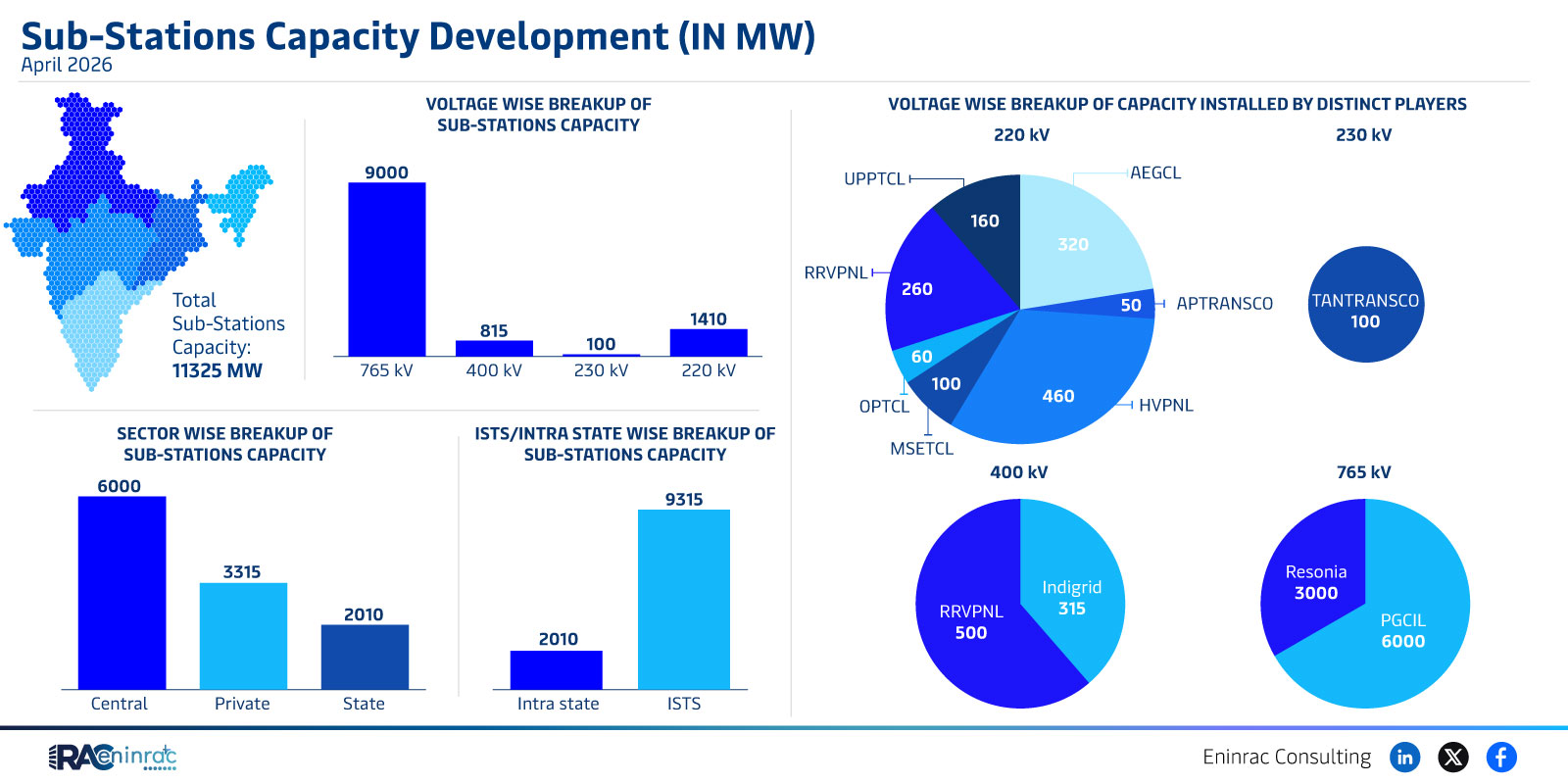

This article examines the sub‑station capacity development data for April 2026, focusing on installed megawatt (MW) capacity across 220kV and 230kV voltage levels. Understanding how capacity is distributed among key players such as AEGCL, APTRANSCO, and TANTRANSCO helps stakeholders gauge infrastructure growth, investment opportunities, and regional power reliability.

What Does the Data Reveal About Sub‑Station Capacity?

The data shows a total installed capacity of 4,815 MW for 220kV and 1,410 MW for 230kV, with a combined capacity of 6,225 MW. Major contributors include AEGCL and APTRANSCO, while TANTRANSCO adds a modest 100 MW. This distribution highlights a stronger focus on 220kV infrastructure, reflecting the demand patterns of central and private sectors.

Voltage‑Level Comparison and Player Contributions

When comparing voltage levels, 220kV sub‑stations dominate with 77 % of total capacity, whereas 230kV accounts for 23 %. AEGCL leads the 220kV segment, while APTRANSCO provides significant capacity across both voltages. TANTRANSCO’s limited 100 MW suggests a niche role, possibly supporting specific regional grids. The data also hints at emerging private sector involvement, as indicated by entries such as "Central Private State Intra state" and consulting firms like Eninrac Consulting.

Impact on Sectors and Industries

Enhanced sub‑station capacity directly influences generation, transmission, and distribution networks. For generators, increased 220kV capacity improves load‑dispatch flexibility and reduces bottlenecks. Transmission operators benefit from a more resilient grid, while distribution companies can deliver reliable power to end‑users. Investors and policymakers can use these insights to prioritize funding, streamline approvals, and encourage private participation in grid expansion.

Key Takeaways

- Total installed capacity for April 2026 reaches 6,225 MW across 220kV and 230kV levels.

- 220kV sub‑stations hold the majority share at 77 % of total capacity.

- AEGCL and APTRANSCO are the primary contributors, driving most of the capacity growth.

- TANTRANSCO adds a modest 100 MW, indicating a focused regional role.

- Private sector and consulting involvement suggest diversification of grid development.

- Capacity growth supports generation stability, transmission reliability, and distribution efficiency.

FAQs

What is the total sub‑station capacity reported for April 2026?

The combined capacity is 6,225 MW, with 4,815 MW at 220kV and 1,410 MW at 230kV.

Which voltage level has the higher installed capacity?

220kV sub‑stations hold the larger share, accounting for about 77 % of total capacity.

Who are the leading players in sub‑station development?

AEGCL and APTRANSCO are the leading contributors, providing the bulk of installed capacity.

Why does TANTRANSCO have a smaller capacity share?

TANTRANSCO’s 100 MW reflects a targeted role, possibly serving specific regional or ancillary grid functions.

How does this capacity data affect investors?

Investors can identify growth areas, assess the strength of key players, and gauge opportunities for private sector participation in grid projects.