Introduction

India’s on‑river and off‑river pumped storage projects represent a critical component of the nation’s renewable energy strategy. As of April 2026, a total of ten operational projects deliver 7,425.6 MW of capacity, while a growing pipeline of construction, examination and survey activities promises to expand the system dramatically. This article breaks down the latest capacity figures, explains what they mean for the power sector, and helps investors, policymakers and energy enthusiasts understand the trajectory of India pumped storage capacity.

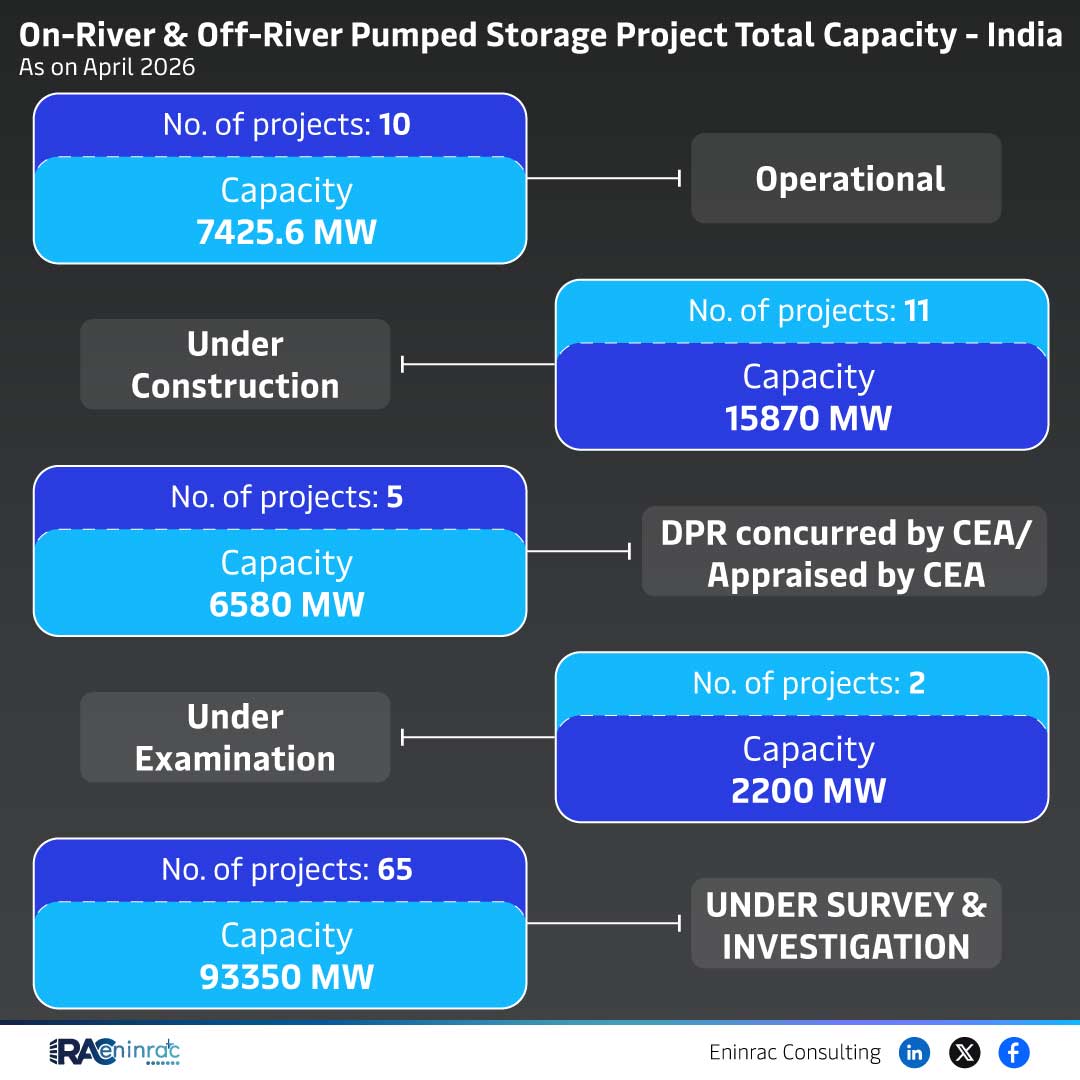

What Does the Data Reveal About This Topic?

The raw data shows four distinct categories of project status: operational, under construction, under examination and under survey or investigation. Operational projects number eleven and contribute 7,425.6 MW. Construction projects total five and aim to add 15,870 MW, with an additional 6,580 MW reported for projects in a later construction phase. Examination activities involve 65 projects with 2,200 MW under review, while survey and investigation efforts cover a massive 93,350 MW, indicating extensive future potential.

Capacity Breakdown by Project Status

When the numbers are compared, construction capacity far exceeds current operational output, suggesting a rapid expansion phase. The 15,870 MW under construction is more than double the operational capacity, and the 6,580 MW figure appears to represent projects that have moved beyond initial groundwork. Examination capacity, though smaller at 2,200 MW, reflects projects awaiting regulatory clearance. The largest figure, 93,350 MW under survey and investigation, signals long‑term planning and feasibility studies that could eventually translate into gigawatts of new pumped storage infrastructure.

Impact on Sectors and Industries

Increased pumped storage capacity enhances grid stability by providing large‑scale energy storage, allowing excess renewable generation to be captured and dispatched during peak demand. This benefits the power generation sector, particularly solar and wind developers who need reliable storage solutions. Transmission operators gain flexibility, and distribution networks experience smoother load curves. For investors, the expanding construction pipeline offers opportunities in civil engineering, turbine manufacturing and ancillary services. Policymakers can leverage the data to shape incentive schemes, renewable integration targets and climate commitments.

Key Takeaways

- Operational pumped storage delivers 7,425.6 MW across eleven projects.

- Construction phase projects aim to more than double current output with 15,870 MW.

- Additional 6,580 MW is slated for later construction stages, indicating staggered rollout.

- Examination activities involve 2,200 MW across 65 projects, pending regulatory approval.

- Survey and investigation cover an ambitious 93,350 MW, highlighting long‑term planning.

- The overall trend points to a rapid increase in India pumped storage capacity, strengthening renewable integration and grid resilience.

FAQs

How much pumped storage capacity is currently operational in India?

As of April 2026, operational projects generate approximately 7,425.6 MW.

What is the total capacity under construction?

Construction projects are slated to add about 15,870 MW, with an additional 6,580 MW in later phases.

What does the examination capacity represent?

Examination capacity of 2,200 MW reflects projects undergoing regulatory and technical review before construction can begin.

Why is the survey and investigation figure so large?

The 93,350 MW under survey indicates extensive feasibility studies for future pumped storage sites, signaling long‑term growth potential.

How does pumped storage support renewable energy integration?

Pumped storage stores surplus renewable electricity and releases it during peak demand, helping balance the grid and reduce reliance on fossil‑fuel peaking plants.